Health insurance policies have become the most essential part of everyone’s financial portfolios. Medical costs are rising unchecked and without a health insurance policy to pay for the bills, a medical contingency seems like a curse. When you have a health insurance policy you are assured of availing quality healthcare facilities as the policy promises to pay for the hospital bills which would incur. It, therefore, spares you the financial horror of a medical contingency and safeguards your savings.

Various health insurance companies in the market offer some of the best policies with comprehensive coverage benefits. However, it is important to judge the claim settlement history of the company. Though health insurance policies promise settlement of your medical bills, if the company does not pay the claim, the policy will not fulfill its promise. That is why the medical claim settlement ratio of the company is required to be checked.

The Insurance Regulatory and Development Authority of India (IRDAI) publishes the Incurred Claims Ratio of health insurance companies after the end of every financial year. This report shows the claims paid by the company against its premium earnings. Let’s understand the concept of Incurred Claims Ratio in detail –

What is the Incurred Claims Ratio?

Incurred Claims Ratio is the ratio of the total amount of claims paid by an insurance company against the total amount of premiums earned.

For example, if in a financial year, the company settles claims of INR 5 crores and earns a premium of INR 8 crores, the Incurred Claims Ratio for that financial year would be [(5/8) * 100] = 62.5%

The formula for calculating the ratio is as follows –

Incurred Claims Ratio = (total amount of claims paid / total amount of premiums collected) * 100

Important aspects of the ratio

Here are some of the important features of Incurred Claims Ratio –

- The ratio is expressed as a percentage. It can be below 100% or even more than that.

- The ratio is calculated taking into consideration the number of claims paid and premiums collected in one financial year. So, if the ratio is for the financial year 2020-21, it would consider the claims paid and premiums collected between 1st April 2020 and 31st March 2021.

- The ratio uses the amount of claim paid vis-à-vis the premium collected. It does not represent the number of policies for which the claim was paid.

- The time taken in settling the claim is not considered in calculating the ratio

Interpreting the Incurred Claims Ratio

The Incurred Claims Ratio depicts the percentage of premium used by the insurance company to pay its claims. The ratio can, therefore, be depicted in the following ways –

- If the ratio is more than 100%, it shows the company is paying more in claims compared to the premiums collected. This shows that the company is making a loss and might face a problem in paying future claims.

- If the ratio is very low, i.e. between 20% and 50%, it shows that the company is earning high volumes of premiums but the claims are very less. This shows that the company is making too much profit. It might also show that the premiums charged by the company are very high which results in a lower ratio. Alternatively, it might also show that the company has a very low claim experience.

- If the ratio is between 60% and 90%, it shows that the company is in a comfortable position to pay its claims. The premiums are not very high and allow the company to generate profits for sustainability. In fact, the ratio in this range is considered to be a good indicator of the company’s solvency.

Claim Settlement Ratio (CSR) & Incurred Claims Ratio (ICR) of Top Health Insurance Companies

Here is a comparative analysis of the Claim Settlement Ratio and incurred Claims Ratio (Health) of top health insurers recorded recently –

|

Name of the insurer |

Health Incurred Claim Ratio (ICR) |

Claim Settlement Ratio (CSR) |

| Acko General Insurance Limited |

84.64% |

97% |

| Aditya Birla Health Insurance Company Limited |

49.08% |

96% |

| Bajaj Allianz General Insurance Company Limited |

77.31% |

98.61% |

| Care Health Insurance Limited |

59.13% |

95.2% |

| Cholamandalam MS General Insurance Company Limited |

77.35% |

56.25% |

| Manipal Cigna Health Insurance Company Limited |

61.13% |

99.96% |

| Edelweiss General Insurance Company Limited |

111.57% |

99.72% |

| Future Generali India Insurance Company Limited |

90.04% |

94.86% |

| Go Digit General Insurance Limited |

63.80% |

– |

| HDFC Ergo General Insurance Company Limited |

99.49% |

– |

| ICICI Lombard General Insurance Company Limited |

78.00% |

– |

| IFFCO Tokio General Insurance Company Limited |

99.49% |

92% |

| Kotak Mahindra General Insurance Company Limited |

55.17% |

98.50% |

| Liberty General Insurance Limited |

76.98% |

94% |

| Magma HDI General Insurance Company Limited |

62.70% |

94.1% |

| National Insurance Company Limited |

101.09% |

– |

| Navi General Insurance Limited |

26.78% |

– |

| Niva Bupa Health Insurance Company Limited |

50.19% |

96% |

| Raheja QBE General Insurance Company Limited |

97.22% |

96% |

| Reliance General Insurance Company Limited |

93.96% |

– |

| Reliance Health Insurance Limited |

45.68% |

– |

| Royal Sundaram General Insurance Company Limited |

67.88% |

– |

| SBI General Insurance Company Limited |

60.72% |

93.09% |

| Shriram General Insurance Company Limited |

4.84% |

95.12% |

| Star Health & Allied Insurance Company Limited |

94.44% |

– |

| TATA AIG General Insurance Company Limited |

67.27% |

– |

| The New India Assurance Company Limited |

92.79% |

– |

| The Oriental Insurance Company Limited |

112.51% |

91.5% |

| United India Insurance Company Limited |

106.04% |

– |

| Universal Sompo General Insurance Company Limited |

111.23% |

90.78% |

(Source: IRDAI)

The top claim settlement ratio for health insurance companies is calculated by the companies themselves based on the annual reports published by the IRDA. IRDA, however, does not publish the best health insurance claim settlement ratios for general insurance companies. The claim settlement ratios are published for life insurance companies only. So, the Incurred Claims Ratio is the best ratio to judge the performance of health insurance companies.

Other important ratios:

Besides the Incurred Claims Ratio, here are some other important ratios which you should consider –

- Claim rejection ratio – This ratio measures the percentage of claims rejected by the insurance company against the total claims made on it. The ratio is calculated as follows –Claim rejection ratio = (number of claims rejected / total claims made) * 100The ratio helps you check the history of claim rejection by an insurance company.

- Pending claim ratio – This ratio shows the number of claims that are pending with the insurance company at the end of the financial year. The formula is as follows –Pending claim ratio = (number of claims pending / total claims made) * 100

- Medical Claim settlement ratio– The claim settlement ratio of health insurance companies is an important ratio that is also advertised by health insurance companies. This ratio measures the number of claims settled by the insurer against the total number of claims made upon it. The calculation is done using the following formula –Medical Claim settlement ratio (number of claims settled / total claims made) * 100

All these ratios give an insight into the efficacy of handling claims by the insurance company. As such, before buying a health insurance policy, these ratios should be checked.

Incurred Claims Ratio vis-à-vis Claim Settlement Ratio of Health Insurance Companies

There is often confusion between the concepts of the Incurred Claims Ratio and the Claim Settlement Ratio of health insurance companies. The claim settlement ratio of health insurance companies is quite a popular concept that measures the number of claims settled by the insurance company. ICR, on the other hand, shows the financial capacity of the company to settle its claims. Other differences between ICR and CSR include the following –

| Incurred Claim Ratio (ICR) | Claim Settlement Ratio (CSR) |

| The ratio is calculated for general insurance companies | The ratio is calculated for life insurance companies |

| The ratio uses the monetary values of claims paid against premiums earned | The ratio uses absolute values of the number of claims paid against the total number of claims made |

Both these concepts are, therefore, different from one another. However, you should check both the ratios when finalising your health insurance policy.

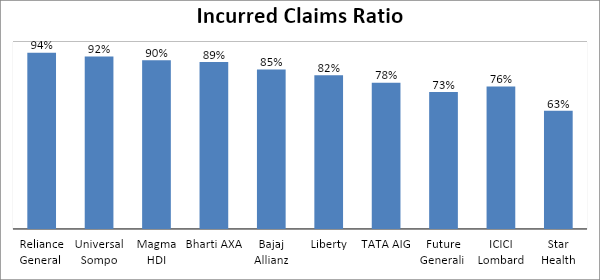

Top health insurance companies in terms of Incurred Claim Ratio:

Here is a graph showing the top ten health insurance providers based on their ICR for the financial year 2017-18 –

How to choose the best health insurance policy?

To choose the best health insurance policy, the incurred claims ratio or the best health insurance claim settlement ratio of the health insurance company should not be the sole parameter. You should judge the policies on the following parameters too –

- The coverage offered – the wider the better

- The premium charged – the lower the better

- Sub-limits or limits on coverage features – as minimal as possible

- Waiting period for pre-existing illnesses – the lower the better

- Value-added benefits – the more the merrier

After comparing the plans on these parameters you should consider the ICR, best health insurance claim settlement ratio, and other relevant ratios discussed above and then make your choice. When you make a well-researched choice of health plan, you will be rewarded with good coverage at affordable premiums. What’s more, your claims would also be settled quickly and smoothly. Isn’t that what you want?

Read more:

- Documents for buying Insurance Policies

- Claim Settlement Ratios for Top-Term Insurance

- Claim Settlement Ratio of Life Insurance Companies

Frequently Asked Questions

1. What is the claim settlement ratio?

Claim settlement ratio is the percentage of claims settled by the insurance company against the total number of claims made against it. So, if an insurance company settles 95 out of 100 claims made on it in one financial year, its claim settlement ratio would be 95%.

2. What is the claim ratio in health insurance?

The claim ratio in health insurance is equal to the claim settlement ratio of an insurance company. It shows the percentage of claims settled by the health insurance company against the total claims made on it in one financial year.

3. What is Incurred Claims Ratio?

Incurred Claims Ratio is the percentage of premiums used up in paying for claims in one financial year. The ratio is measured as the amount of claims paid in one year against the amount of premiums earned by the insurance company. So, if an insurance company earns INR 100 in premiums and pays INR 75 in claims, the incurred claims ratio would be 75%.

4. What is the difference between Incurred Claims Ratio & claim settlement ratio

Both these ratios measure different things. The claim settlement ratio (CSR) measures the number of claims settled by the insurance company against the total claims made. The incurred claims ratio (ICR), on the other hand, measures the amount of premium used to pay the claims. While the CSR shows the goodwill of the company in paying its claims, the ICR shows the financial standing of the company. The CSR can never be greater than 100% but the ICR can be. Moreover, a high CSR is desirable but a high ICR shows that the company is paying most of its premiums for claims and is a bad indicator of the company’s financial standing.

Found this post informational?

Browse Turtlemint Blogs to read interesting posts related to Health Insurance, Car Insurance, Bike Insurance, and Life Insurance. You can visit Turtlemint to Buy Insurance Online.

from Day 1")